Starting an HVAC business offers significant earning potential in an industry where demand for skilled professionals consistently outpaces supply. However, launching a legitimate operation requires more than technical expertise. Three foundational pillars determine whether your business will survive its first year and thrive beyond it: licensing, insurance, and equipment. Each element serves a distinct purpose. Licensing establishes your legal authority to operate and signals competency to customers. Insurance shields your business from financial catastrophe. Equipment enables you to deliver quality work efficiently. Cutting corners on any of these three areas exposes you to fines, lawsuits, and reputational damage that can end a business before it gains traction. This guide breaks down the specific requirements, costs, and strategies for each pillar so you can build your HVAC business on solid ground.

Licensing Requirements for HVAC Businesses

HVAC licensing is the process through which a state, county, or municipal authority grants legal permission to an individual or company to perform heating, ventilation, air conditioning, and refrigeration work. Licensing exists to protect consumers by verifying that practitioners meet minimum standards of competency and professionalism.

State vs. Local Licensing

Licensing structures vary dramatically across the United States. Some states maintain centralized, statewide licensing systems. Florida, for example, requires HVAC contractors to hold a state-issued license through the Department of Business and Professional Regulation. California mandates a C-20 (Warm-Air Heating, Ventilating and Air-Conditioning) license through the Contractors State License Board. Texas requires an ACR (Air Conditioning and Refrigeration) contractor license through the Texas Department of Licensing and Regulation.

Other states, such as Colorado, Illinois, and Pennsylvania, defer licensing authority to local jurisdictions. In these states, requirements can differ significantly between cities and counties. If you plan to operate across multiple jurisdictions, you must verify requirements for each area where you intend to work.

Types of HVAC Licenses

- Contractor License: This top-tier license authorizes you to bid on projects, manage jobs, hire employees, and pull permits. It is the license you need to own and operate an HVAC business. Most states require several years of documented experience and passing both technical and business law examinations.

- Journeyman or Technician License: This license allows individuals to perform HVAC work under the supervision or employment of a licensed contractor. It typically requires completion of an apprenticeship or equivalent experience (usually 3 to 5 years) and passing a technical exam.

- Specialty Licenses: Some jurisdictions issue separate licenses for refrigeration, ductwork installation, hydronic heating, or other specialized HVAC disciplines.

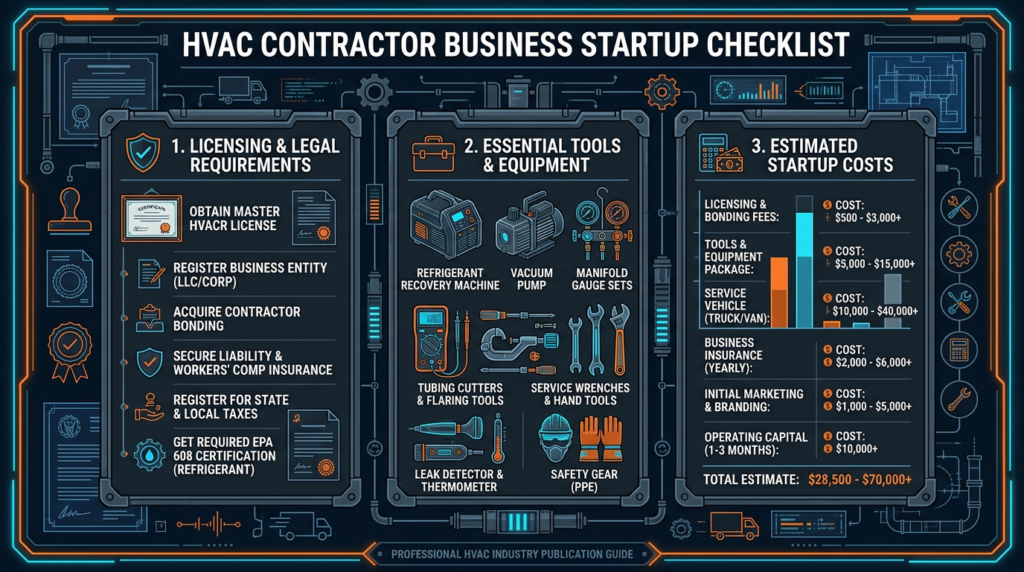

- EPA 608 Certification: Federal law requires anyone who handles refrigerants to hold EPA Section 608 certification. This is not optional and applies regardless of state licensing. The certification has four categories: Type I (small appliances), Type II (high-pressure systems), Type III (low-pressure systems), and Universal (all types). Most HVAC professionals pursue Universal certification. Violations for improper refrigerant handling carry fines up to $44,539 per day per violation under the Clean Air Act.

What You Need to Get Licensed

Education: Most states require a combination of formal education and practical training. Trade school programs, community college HVAC programs, and registered apprenticeships all count. NATE (North American Technician Excellence) certification, while not always legally required, strengthens your application and credibility. Some states accept NATE certification as partial fulfillment of licensing requirements.

Experience: States typically require between 2 and 5 years of documented work experience under a licensed contractor before you can apply for a contractor license. Florida requires 4 years, Texas requires 5 years, and California requires 4 years of journey-level experience. Keep meticulous records of your work hours, employer information, and job descriptions. Gaps or poor documentation are among the most common reasons applications get denied.

Examinations: Expect to pass at least one technical exam covering HVAC system design, installation, troubleshooting, and code compliance. Many states also require a separate business and law exam covering contract law, lien law, and permit requirements. Study resources include state-published candidate handbooks, online prep courses, and review materials from organizations like ACCA (Air Conditioning Contractors of America).

Background Checks: An increasing number of states require criminal background checks as part of the licensing process. Felony convictions, particularly those involving fraud or theft, can delay or prevent licensure.

Maintaining and Renewing Your License

Licenses are not permanent. Most states require renewal every 1 to 3 years, with continuing education units (CEUs) as a condition of renewal. Florida requires 14 hours of continuing education per renewal cycle. Texas requires 8 hours annually. CEU topics often include code updates, safety practices, and new technology.

License reciprocity between states is limited but does exist in some cases. States with similar licensing standards may honor out-of-state credentials, sometimes with additional requirements. For example, some states participate in interstate compacts or allow expedited licensing for military veterans with equivalent training. Always verify reciprocity agreements directly with your target state’s licensing board.

Consequences of Operating Without a License

The risks of operating unlicensed are severe. Penalties include fines ranging from $500 to $10,000 or more per violation, criminal misdemeanor or felony charges depending on the state, court-ordered business closure, and inability to enforce contracts or collect payment for completed work. Unlicensed contractors also cannot obtain commercial insurance, leaving them personally liable for any damages or injuries.

Insurance Requirements for HVAC Businesses

Business insurance protects your HVAC company from the financial consequences of accidents, injuries, property damage, and legal claims. Without adequate coverage, a single incident can bankrupt a startup. Many states and municipalities require proof of insurance before issuing or renewing a contractor license.

Essential Types of Insurance

General Liability Insurance: This is the foundation of your insurance program. It covers third-party claims for bodily injury, property damage, and advertising injury. If a technician accidentally damages a customer’s ceiling during a ductwork installation or a passerby trips over equipment at a job site, general liability pays for the resulting claims and legal defense. Most HVAC businesses carry $1 million per occurrence and $2 million aggregate. Annual premiums typically range from $500 to $3,000 for small operations.

Workers’ Compensation Insurance: Nearly every state requires businesses with employees to carry workers’ compensation. This coverage pays medical expenses and a portion of lost wages when an employee is injured on the job. HVAC work involves significant hazards including electrical shock, burns, falls, and refrigerant exposure, making this coverage critical. Penalties for non-compliance vary by state but can include fines of $1,000 per day of non-coverage, criminal charges, and personal liability for all employee medical costs. Premiums depend on payroll size, claims history, and the classification codes assigned to your work.

Commercial Auto Insurance: Personal auto insurance policies do not cover vehicles used for business purposes. If your technician causes an accident while driving a company van to a service call, your personal policy will deny the claim. Commercial auto insurance covers liability and physical damage for business vehicles. Required minimum coverage varies by state but typically starts at $500,000 in combined single-limit liability. Premiums depend on fleet size, driver records, vehicle types, and coverage limits.

Professional Liability Insurance (Errors and Omissions): If your business provides system design, energy audits, or consulting services, professional liability insurance covers claims arising from negligent advice, design errors, or failure to perform services as promised. This is particularly important for commercial HVAC contractors handling complex system specifications.

Surety Bonds: A surety bond is a financial guarantee that you will fulfill your contractual obligations. Many states require HVAC contractors to post a surety bond as a licensing condition. Bond amounts vary: California requires a $15,000 contractor bond, while other states require $5,000 to $25,000. If you fail to complete a project or violate regulations, the bond compensates the affected party. You pay an annual premium, usually 1% to 15% of the bond amount, based on your credit score.

Inland Marine Insurance: HVAC technicians transport expensive tools and equipment in their vehicles daily. Inland marine insurance covers tools, diagnostic equipment, and materials while in transit or stored at job sites. Standard commercial property policies typically exclude coverage for items away from your primary business location.

Commercial Property Insurance: If you own or lease a shop, warehouse, or office, property insurance covers damage from fire, storms, theft, and vandalism. It also covers your inventory of parts and materials stored at that location.

Determining Your Coverage Needs

Your insurance requirements depend on the size of your operation, number of employees, types of services offered, and geographic location. A sole proprietor performing residential maintenance has different needs than a 20-person company handling commercial installations. Work with an insurance broker who specializes in construction trades or HVAC businesses. They understand the specific risks and can identify coverage gaps you might overlook.

Strategies for Managing Insurance Costs

- Obtain quotes from at least three insurance carriers before purchasing.

- Bundle multiple policies with one carrier for volume discounts.

- Maintain a clean claims history by prioritizing workplace safety.

- Increase deductibles to lower premium costs, but only if you can absorb the out-of-pocket expense.

- Implement formal safety training programs. Many insurers offer premium discounts for documented safety programs.

- Review policies annually as your business grows to ensure coverage remains adequate.

Common Insurance Misconceptions

Many new business owners believe they do not need insurance because they are careful or because they work alone. Accidents are unpredictable, and a single liability claim can exceed $100,000. Others assume personal auto insurance covers their work truck, which it does not. Solo operators sometimes believe they are exempt from workers’ compensation, but requirements vary by state, and some states mandate coverage even for the business owner.

Equipment Requirements for HVAC Startups

Your tools and equipment directly affect the quality, speed, and safety of your work. Investing in the right equipment from day one prevents costly rework, improves diagnostic accuracy, and builds customer confidence.

Hand Tools

Every HVAC technician needs a comprehensive set of hand tools including adjustable wrenches, hex key sets, pliers (needle-nose, channel-lock, and lineman), screwdrivers (flathead and Phillips in multiple sizes), pipe cutters, tubing benders, flaring tools, wire strippers, and tape measures. Invest in commercial-grade tools from established manufacturers. Budget tools fail faster and can compromise workmanship. A quality hand tool set costs between $1,500 and $3,000.

Power Tools

Essential power tools include a cordless drill/driver, impact driver, reciprocating saw, rotary hammer for masonry work, and a metal shear for ductwork. Cordless platforms from major manufacturers like Milwaukee, DeWalt, or Makita offer interchangeable batteries across tools, reducing overall investment. Budget $2,000 to $4,000 for a solid power tool lineup.

Diagnostic and Testing Equipment

Accurate diagnostics separate professionals from amateurs. Essential instruments include a quality digital multimeter, a refrigerant manifold gauge set (digital manifolds with Bluetooth connectivity offer faster, more accurate readings), a combustion analyzer for furnace testing, manometers for static pressure measurement, temperature probes, an anemometer for airflow measurement, and a leak detector for refrigerant systems. A thermal imaging camera is increasingly expected for identifying insulation gaps, duct leaks, and electrical hotspots. Diagnostic equipment costs between $3,000 and $8,000 depending on the brands and features you select.

Refrigerant Handling Equipment

EPA regulations require proper recovery, recycling, and reclamation of refrigerants. You need a refrigerant recovery machine, a vacuum pump (at minimum 4 CFM for residential work), a digital refrigerant scale, and a micron gauge for evacuation verification. Budget $2,000 to $4,000 for this category.

Safety Equipment

OSHA requires employers to provide appropriate personal protective equipment (PPE). Stock safety glasses, work gloves, electrical-rated gloves, hearing protection, respirators, hard hats, and fall protection equipment for rooftop work. Keep a first aid kit in every service vehicle. Safety equipment costs roughly $500 to $1,500 per technician.

Vehicles

A reliable service vehicle is one of your largest startup expenses. Cargo vans (Ford Transit, RAM ProMaster, Mercedes Sprinter) or pickup trucks with utility beds are standard. Factor in shelving and organization systems to protect tools and maximize storage. Used vehicles in good condition cost $20,000 to $35,000, while new vehicles range from $35,000 to $55,000 depending on configuration.

Leasing vs. Buying Equipment

Purchasing equipment outright builds equity and eliminates ongoing payments, but it requires significant upfront capital. Leasing preserves cash flow and may offer tax advantages since lease payments are typically deductible as business expenses. For high-cost items like vehicles and expensive diagnostic equipment, leasing can make sense during the first year. For hand tools and commonly used instruments, buying is almost always more cost-effective.

Technology and Software

Modern HVAC businesses rely on technology beyond the toolbox. Field service management software handles scheduling, dispatching, invoicing, and customer communication. Platforms like ServiceTitan, Housecall Pro, and Jobber streamline operations and reduce administrative overhead. Bluetooth-enabled gauges and digital manifolds that connect to smartphones allow technicians to record and share data instantly. Budgeting $100 to $300 per month for software is standard for small operations.

Common Mistakes and Pitfalls

- Operating without proper licensing: Even if you have years of experience, performing work without the required license exposes you to fines and legal action. Verify requirements before accepting your first job.

- Under-insuring the business: Minimum coverage is not always adequate coverage. One major claim can exceed a bare-bones policy limit and leave you personally responsible for the difference.

- Skipping equipment maintenance and calibration: Inaccurate gauges lead to improper refrigerant charges. Dull tools produce sloppy work. Establish a maintenance and calibration schedule from day one.

- Ignoring EPA and OSHA regulations: Federal regulations apply to every HVAC business regardless of size. Non-compliance results in fines, work stoppages, and potential criminal liability.

- Failing to seek professional advice: Consult with an attorney for business formation and contract review, an accountant for tax planning, and a specialized insurance broker for coverage design. These upfront costs prevent far more expensive problems later.

Key Takeaways

Launching an HVAC business requires a disciplined approach to three critical areas. Licensing establishes your legal authority to operate, requires documented experience and examination, and varies by state and locality. Insurance protects your investment from the unpredictable risks inherent in HVAC work, with general liability, workers’ compensation, and commercial auto forming the minimum coverage baseline. Equipment represents your ability to deliver quality work, with a realistic startup investment ranging from $30,000 to $80,000 depending on whether you buy new or used vehicles and tools.

Begin by researching the specific licensing requirements in your state and municipality. Contact your state licensing board directly for the most current information. Engage an insurance broker with experience in the HVAC or construction trades. Develop a detailed equipment list based on the services you plan to offer, and prioritize quality over quantity. The HVAC industry rewards professionals who invest in doing things right from the start, and the businesses that last are the ones built on a foundation of compliance, protection, and capability.